Proposal activity for architecture, engineering and construction industry firms remained historically strong in the third quarter, despite a slight easing in some sectors and submarkets.

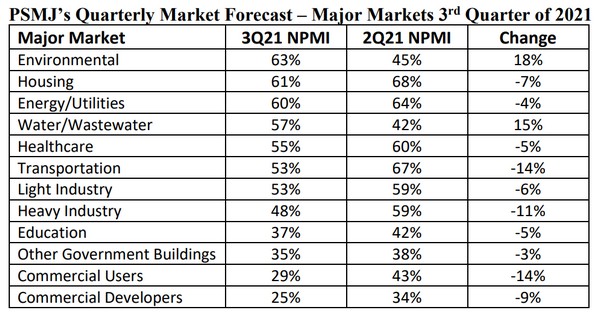

The environmental market led the 12 major markets with a third quarter net plus/minus index of 63%, followed by housing (61%), energy/utilities (60%), water/wastewater (57%) and healthcare (55%).

The environmental market led the 12 major markets with a third quarter net plus/minus index of 63%, followed by housing (61%), energy/utilities (60%), water/wastewater (57%) and healthcare (55%).

While healthcare recorded the fifth-highest level of activity among the 12 major markets, the submarkets indicate an increase of 11% from second quarter for medical labs (51%) and 4% for hospitals (47%), no change for medical office buildings (50%) and a decrease of -4% for continuing care facilities (43%).

Overall proposal opportunity NPMI slipped to 38% from its record-setting level of 52% in the second quarter, but it still marked the third-highest third quarter NPMI in the 18-year history of PSMJ’s Quarterly Market Forecast (just behind 41% in 2005 and 40% in 2018).

PSMJ’s NPMI expresses the difference between the percentage of firms reporting an increase in proposal activity and those reporting a decrease.

“Every major market has now recovered from the COVID dip and all see increasing proposal activity,” says PSMJ Senior Principal David Burstein, P.E., AECPM. “The markets that have seen the biggest improvement in the past year are education and industrial. Of the 58 submarkets we track, only office buildings and retail buildings continue to lag. Unless a new vaccine-resistant COVID-19 strain emerges, we see no impediments to continuing this strong market performance.”