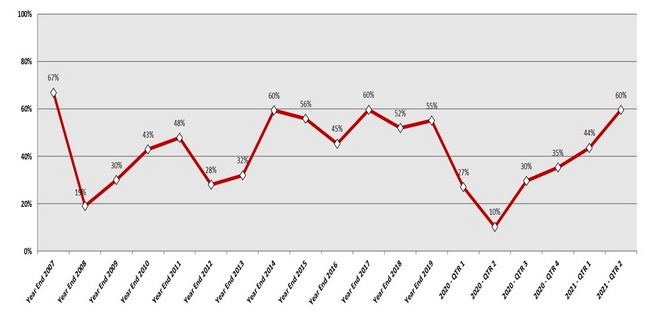

Proposal activity in the healthcare market accelerated in the 2nd quarter, according to the PSMJ Resources Quarterly Market Forecast survey of architects, engineers and contractors. Among participants working in the healthcare space, 64% said they experienced an increase in proposal opportunities in the second quarter when compared with the first quarter. Only 4% said they saw a decrease, resulting in a net plus/minus index of 60%.

For each quarter of 2019 and 2020, healthcare’s net plus/minus index ranked among the three hottest major markets of the 12 included in the PSMJ survey. That streak ended in the first quarter of 2021, as healthcare slid to a tie for 7th. In the second quarter, healthcare’s NPMI was third-highest among major markets, and its increase of 16 NPMI percentage points was tied for best, as well.

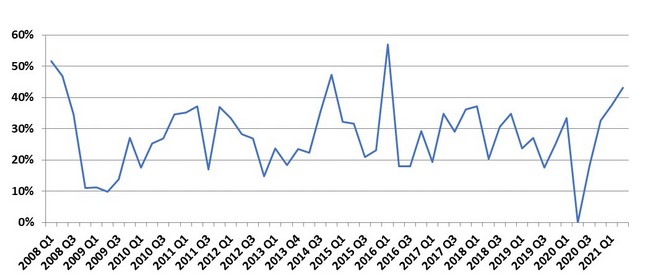

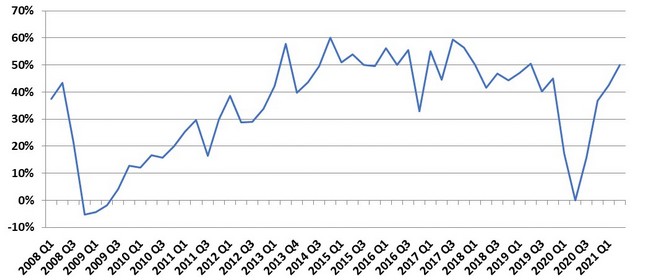

All four healthcare submarkets also reported high levels of proposal activity. Medical office buildings recorded an NPMI of 50%, which is 8 NPMI percentage points higher than the first quarter. Continuing care facilities slid 8 NPMI percentage points to a still-solid 47% NPMI, while hospitals (43% NPMI, up 5 percentage points) and labs 40%, up 2) round out the healthcare submarket results.

Senior/assisted living, a submarket included under the housing market, had an NPMI of 49% in the second quarter, down from 59% in the first quarter.

Healthcare Market Proposal Activity – 2007 to 2021 (NPMI)

PSMJ’s NPMI expresses the difference between the percentage of firms reporting an increase in proposal activity and those reporting a decrease. The QMF has proven to be a solid predictor of market health for the A/E/C industry since its inception in 2003. A consistent group of over 300 firm leaders participate in the quarterly survey.

Hospital Submarket Proposal Activity – 2008 to 2021 (NPMI)

Medical Office Buildings Submarket Proposal Activity – 2008 to 2021 (NPMI)

For more information, visit https://www.psmj.com/surveys/quarterly-market-forecast-2.