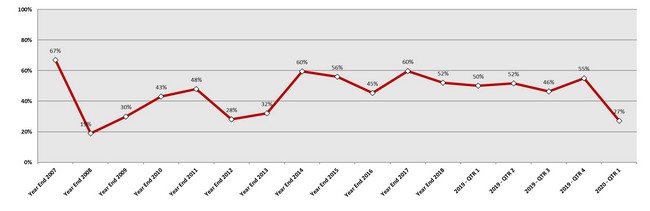

Proposal activity for U.S. Healthcare facilities remained relatively robust in the 1st quarter of 2020, despite the COVID-19 crisis’ devastating effect on the economy and many other markets served by the architecture, engineering and construction industry.

As reported by survey participants in PSMJ’s Quarterly Market Forecast, Healthcare’s Net Plus/Minus Index of 27% marked its second consecutive quarter as the top market for proposal opportunities. Of the 12 markets analyzed in the survey, healthcare was one of only four in positive territory.

PSMJ’s NPMI expresses the difference between the percentage of firms reporting an increase in proposal activity and those reporting a decrease. A consistent group of over 300 firm leaders participate regularly, with 288 contributing to the most recent survey, conducted from March 22-31.

Though it remained on top, healthcare’s NPMI dropped substantially from the 2019 high of 55% in the 4th quarter. Nearly 61% of respondents reported growth in healthcare proposal activity during the final quarter of last year, while only 5.8% reported weakening conditions. In the 1st quarter survey, the percentage seeing an increase dropped to 43.8%, and those reporting a decrease nearly tripled to 16.7%.

Healthcare Market Activity – 2007 to 2020

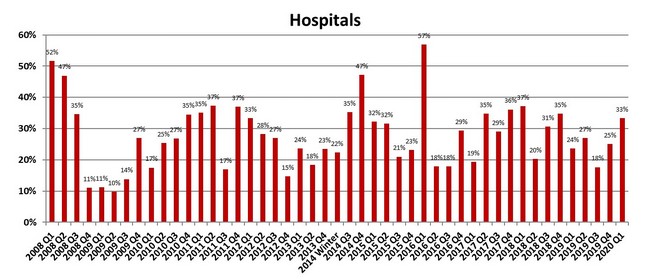

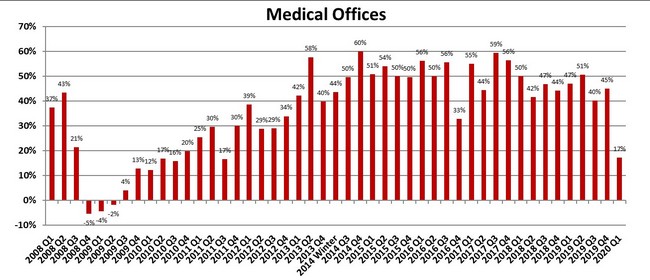

Hospitals (33%) recorded the highest NPMI of all 58 submarkets measured across all major markets, followed by medical labs (27%) and continuing care facilities (27%). The medical office building submarket (17%) was 10th, as its activity slumped as the focus moved to more urgent areas of the industry.

“Firms that work in healthcare haven’t seen opportunities dry up as much as they’ve had work shift toward helping their clients address this crisis,” says PSMJ Consultant Greg Hart, who manages the QMF. “As a result, people in the healthcare practices of some firms are busier than ever right now.”

Water/wastewater (NPMI of 24%) is the other major market that seems to be weathering the COVID-19 storm. It was followed by transportation (7%), energy/utilities (1%) and environmental (-5%) among the 12 major markets measured. The commercial developer (-51%) and commercial user (-47%) markets were the worst performers in the 1st quarter, with lows unseen since the Great Recession.